Features | Editorial | 5 Mins Read | by AG Latto

Good funds own good stocks. The funds run by Woodford Investment Management owned bad stocks. The end game may have only been a matter of time.

Most stocks underperform over their lifetimes.

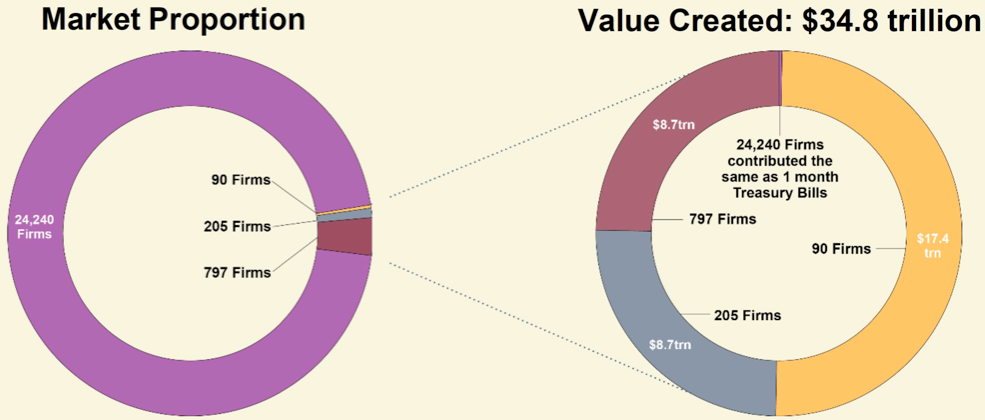

This is highlighted in a research paper covering 25,332 US stocks from 1926 to 2016 – Do Stocks outperform Treasury Bills? (Bessiminder)

- A total of 24,240 firms (95.7%) collectively matched the return of 1-month Treasury bills - 22 out of 23 stocks.

- The top 1,092 (4.3%) of firms generated the market's outperformance versus 1-month Treasury Bills - 1 out of 23 stocks.

- The top 90 (0.36%) of firms generated over half the market's outperformance versus 1-month Treasury Bills – 1 out of 281 stocks.

The message is clear - it pays to be selective when it comes to stock investing.

Total wealth created by all listed US common stocks 1926-2016

Source: Baillie Gifford presentation

Contrarian and value investing

Contrarian and value investors focus on the 95.7% of stocks that collectively match 1-month Treasury Bills over their lifetimes. These are stocks that are cheap for a reason.

The approach is that it is a zero-sum game. A contrarian manager only does well if another manager loses money i.e. a contrarian buys a stock that someone else has lost money on.

Investors cannot collectively do well by investing in the 95.7% of stocks that match 1-month Treasury Bills.

A contrarian/value manager may be able to outperform if they have the best research team. But the approach carries significant blow up risk.

In my view, it is possible for almost any contrarian/value manager can blow up. Think of Neil Woodford today or Bill Miller during the financial crisis.

Bill Miller bet on financials in 2007/2008 and lost his shirt. Woodford recently bet on a series of low companies that have often blown up.

Value and contrarian managers find that their luck runs out at some point.

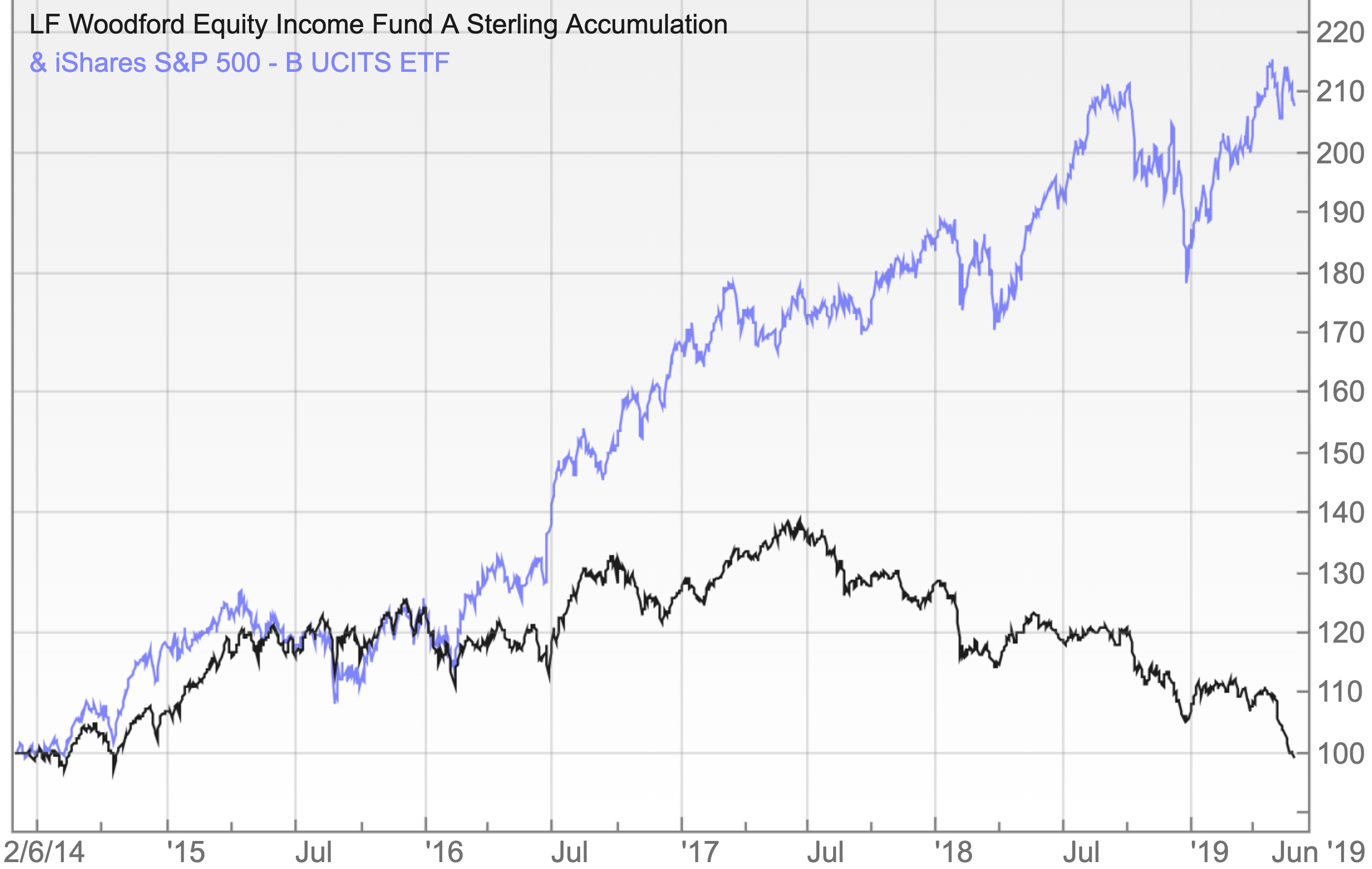

Woodford against the iShares S&P 500 ETF (CSP1)

Source: SharePad

Woodford Investment Management – look at the stocks

Fund analysis can be over complex and personality driven.

Looking at the stocks in a fund is the only way that works. It provides an early-warning signal that a manager is going off the rails.

Woodford’s risky bets on early-stage companies raised eyebrows.

The best venture capitalists find it hard to generate strong returns. You need one big winner to offset lots of losers.

Some would say that Woodford IM has been unlucky. But the manager also bought into mature businesses that have experienced issues.

The lesson, in my view, is that you have to understand the stocks in a fund.

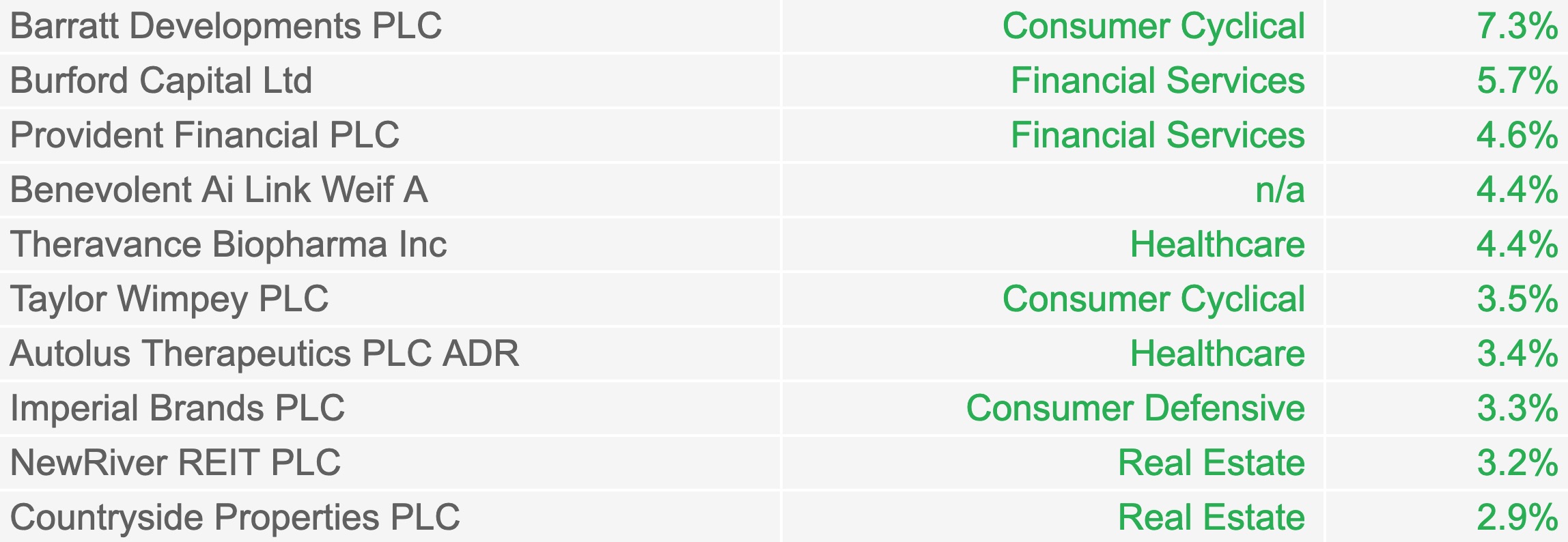

Woodford Equity Income - Not what I would call good stocks

Source: SharePad, Woodford Equity Income A at end of March 2019

Passive versus active

Some will say that the Woodford debacle reinforces the case for passive management. There is some merit to this argument.

It is only worth going for an active fund if it can beat the best available passive fund.

Passive management ensures you own the long-term winners that drive the market.

The case for active management is based on a manager identifying long-term winners.

In other words, whether a fund manager can pick the stocks that drive the market. The best stocks are the 0.36% or 1 in 281 that generate the majority of the market's outperformance against Treasury Bills.

The best active funds seek the best long-term stocks. They don't try to be clever. They hold the best stocks for the long-term.

Quality investing

The quality investment style has the most promise, in my view. However, it is not without risk.

Quality stocks need to be quality stocks. Blow up risk is not something that can be modelled – it is a judgement call.

A salient example is the relatively lacklustre return generated by the Fundsmith Emerging Market Equity Fund. Emerging market stocks often go awry.

The Woodford fan club

Few come out of the Woodford episode with flying colours.

I have never understood why stock analysis isn't used to assess funds. An equity analyst I know was told, when applying for a job evaluating funds, that stock analysis isn't relevant.

Most research on funds that I have read seems to be two stages 1) talk to the manager 2) repeat what they have said. It is not clear how this adds any value.

People seem to have been deluded by the cult of personality.

At a recent fund event I attended in May 2019 a speaker refused to criticise Woodford IM. They stated that the best time to invest in a fund is when it is doing badly.

Just a few simple principles can help when selecting the best funds - both active or passive.

The approach this website uses is to look at three criteria 1) where a fund invests 2) how it invests and 3) who is investing.

Woodford Investment Management wouldn't have gotten past the first stage. It generally makes sense for large equity funds to have a global mandate.

It also makes sense to look at the stocks in a fund. This is one of the first things that I do.

The rules

It is not clear why an open-end fund can invest in unlisted securities. It is enough of a challenge when open-end funds invest in illiquid, small cap stocks.

Summary

Woodford Investment Management has learnt the cost of not being sufficiently selective. Buying contrarian/value stocks works......until it doesn’t.

Fund investors also need be selective when considering funds.

The default option is a passive fund that contains good companies.

Active funds need to be treated with caution. The value/contrarian style has meaningful risk of blowing up.

Active funds that invest in high quality stocks may have the best chance of doing well - they are swimming with the stock market tide. Other fund managers are swimming against the tide.