Fund Stocks | 5 Mins Read | by AG Latto

Currently the second biggest FTSE 100 stock, Unilever is the UK's largest quality company. It is also the biggest position in the Lindsell Train Global Equity Fund at 8% of assets.

The investment case for the stock is covered in this month's Master Investor Magazine.

PDF - UnileverMasterInvestor2019

Master Investor Magazine

Unilever's investment case

Unilever may be the UK's most attractive stock for investors seeking a reliable income. The company pays a quarter dividend that is 1.5X covered by earnings.

Demand for Unilever's products is resilient. The business is also diversified by product line and geography. Emerging markets underpin the long-term growth outlook and generate 59% of revenue.

Unilever may be one of the lowest risk ways to buy into the emerging market growth story. India, China, Brazil and Indonesia generated 25% of Unilever's revenue in 2018.

The most important emerging market for the group is India at 9% of revenue. When the takeover of Horlicks (India) completes, this will increase to around 10%.

Unilever is the market leader in beauty and personal care in India. It has the number one positions in skin cleansing, skin care hair care and makeup.

Unilever's changing business mix

Unilever has traditionally been seen as a food business and has previously been listed in the food products sub-sector. The company is now driven by its beauty and personal care division.

The change in business mix is improving Unilever's profit margin and growth profile. Brand loyalty for cosmetics and personal care products is stronger than it is for food.

Unilever's twelve brands generating over €1bn in annual revenue

Source: Unilever

The valuation conundrum

While Unilever's margins are improving, the pace of underlying sales growth has weakened. The company is having a hard time selling more of its products in Europe and North America.

Against this backdrop, the P/E ratio that the shares trade on has increased in recent years. Does a company with a targeted growth rate of 3-5% merit an historic P/E ratio of 20X earnings?

Companies with equally robust business franchises are generating stronger growth. They include US tech giants like Facebook, Alphabet and Microsoft.

Unilever's P/E based on the last 12 month's reported earnings

Source: SharePad

Acquisitions

A number of Unilever's acquisitions have raised eye brows. Dollar Shave Club was taken over as a loss making business; it is unclear if it will ever become profitable. Horlicks has a well established brand in India but the takeover valuation was high.

One objective for Unilever's acquisitions is to increase the overall pace of revenue growth. But Unilever's underlying sales growth has been declining since 2012.

A steady compounder

Most companies fail. One reason that Unilever is valued by investors is because it should be able to stand the test of time.

Unilever doesn't face the risks that may impact its FTSE 100 peers. Shell, BP, HSBC, Rio Tinto and Vodafone are at risk from increasing regulation, banking fines, cyclical demand and commodity prices.

With over 400 brands, Unilever should be able to offset headwinds in any one area. It is generally the unexciting stocks that perform best over the long term.

Unilever is the investment tortoise competing against racier investment hares. It seems obvious that the hares will win, but the plodding tortoise emerges triumphant.

The shares will therefore tend to perform best on a relative basis when economic and market setbacks take hold. In periods of strong economic growth, we are likely to see investors flock to racier parts of the market.

A business we can understand

Another advantage of Unilever is that it is easy to understand. We use its products as consumers and can see when the competition is making inroads. This kind of research is known as scuttlebutt.

Tesco, for example, has launched an own-brand product to compete with Marmite. I have chosen to stick with Marmite for now.

Summary

Unilever is not exciting but that is part of its appeal. If the company can increase underlying revenue growth to the the upper end of its 3-5% target, the shares should perform well.

It is hard to think of a lower risk way to buy into the emerging market story. Other funds and stocks with emerging market exposure have often come unstuck.

Key risks facing the company include emerging market volatility and the long term durability of its consumer brand portfolio. Will the appeal of Dove, Lipton, Axe, Magnum and Hellmann's endure for decades to come?

Additional comment below

Unilever versus emerging market funds

Unilever is one of the most diversified businesses listed on the London Stock Exchange. It is similar to a fund in the sense that the company is made up of different divisions and brands.

It is interesting to compare Unilever's performance to a number of different investment funds.

Fundsmith Equity Fund (FEET)

One way to invest into emerging markets is to buy emerging market stocks. It is hard to do this directly but there are funds that invest in emerging markets.

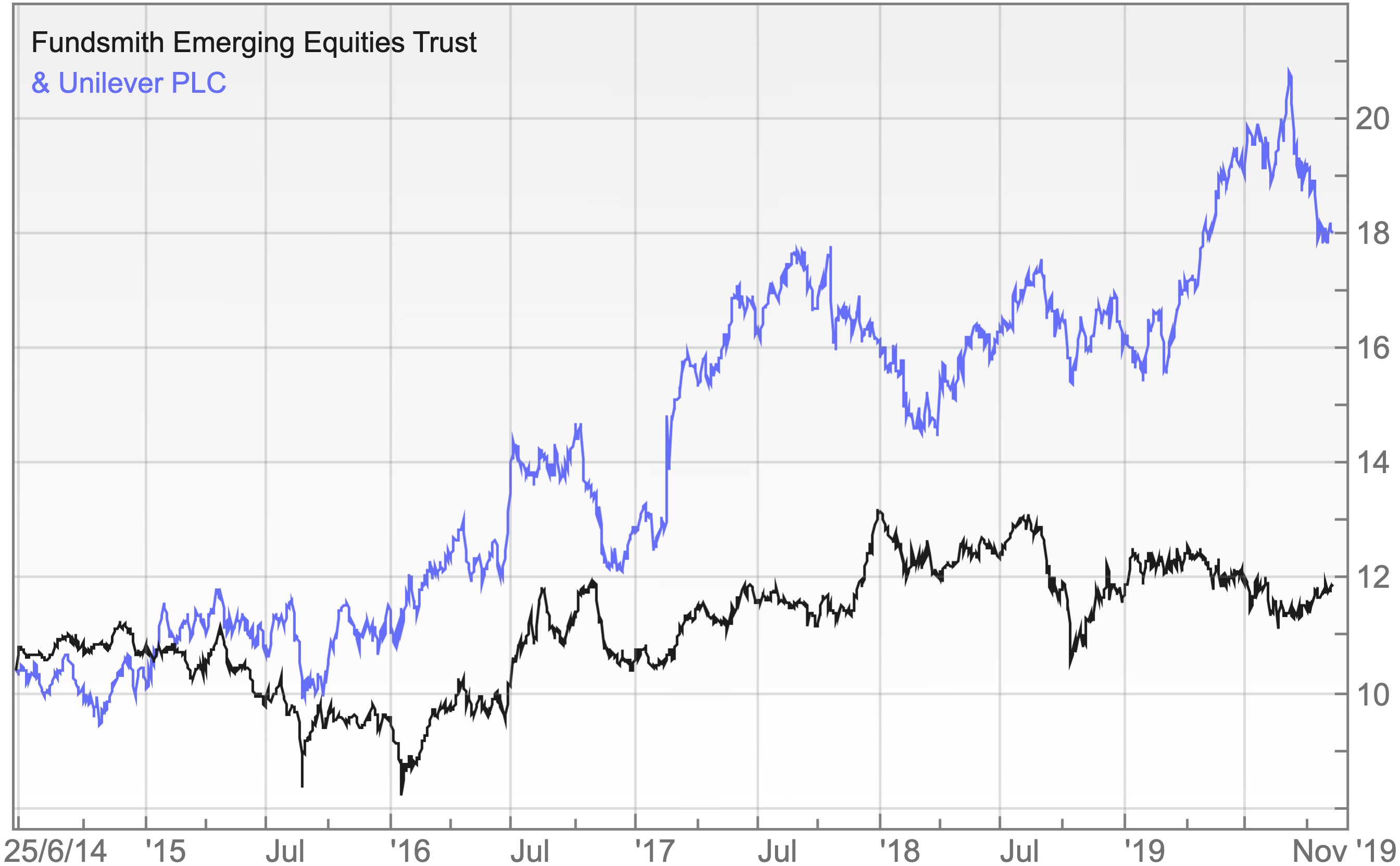

Fundsmith Emerging Equities Trust (FEET) seeks to buy high quality companies that are listed in emerging markets. The consumer staples sector accounted for 62% of the fund's net asset value at the end of September 2019.

It is notable, though, that Unilever outperformed FEET since was launched in June 2014. Unilever has also been an attractive dividend payer over this period.

Unilever beats FEET

Source: SharePad

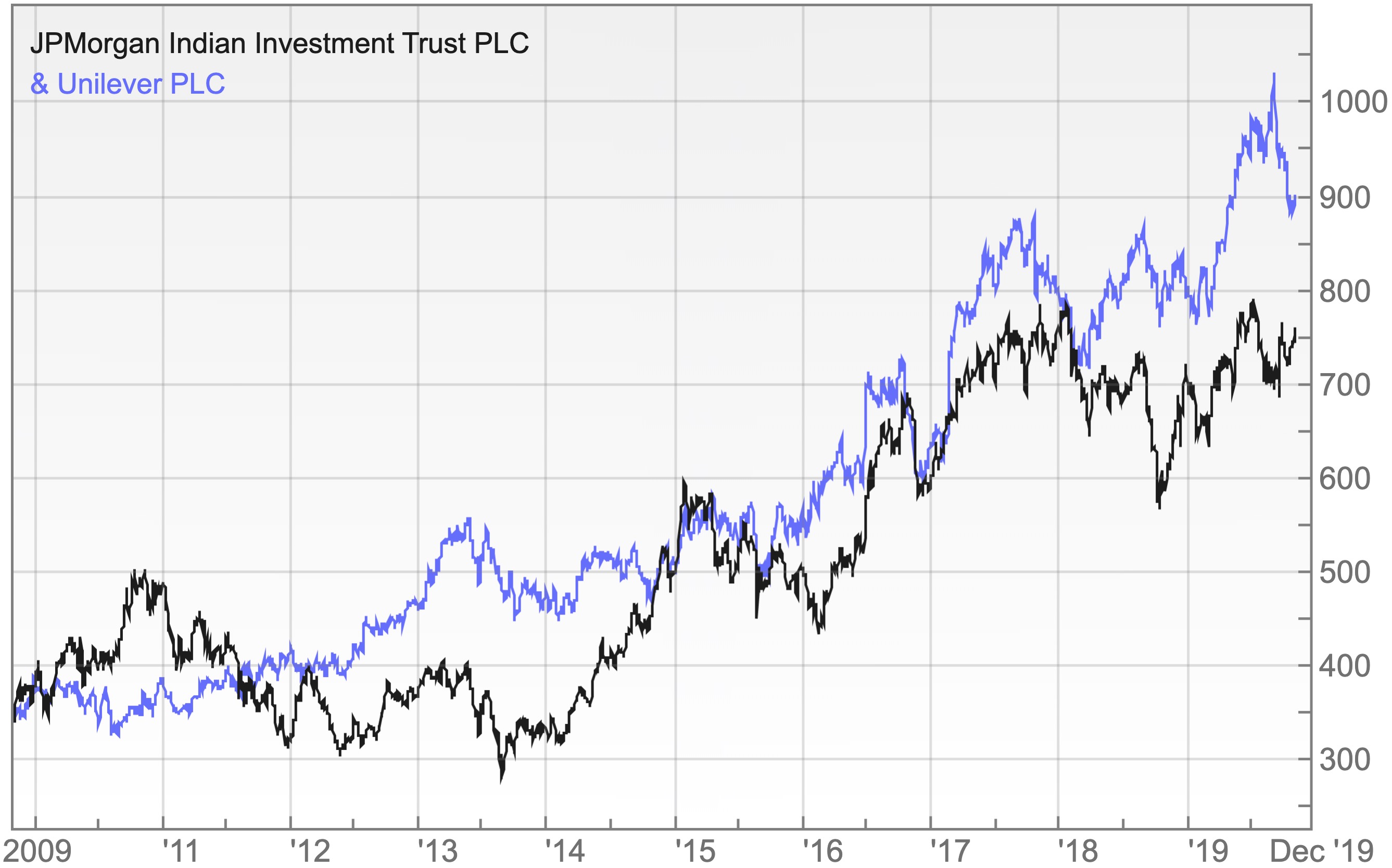

It is also notable that Unilever has outperformed the JP Morgan India Investment Trust (JII) over the last 10 years. JII doesn't pay a dividend while Unilever's dividend yield has tended to be over 3%.

In theory, emerging market funds should outperform because they are buying faster growing businesses. In practice this hasn't been the case. The investment tortoise has won the day.

Unilever outperforms the JP Morgan India Investment Trust

Source: SharePad