General Stocks | 8 Mins Read | by AG Latto

The US fitness group Peloton publicly filed for its IPO on 27th August. The company is growing fast but lost $195.6 million in the year to June 2019. From an investing perspective, the anti-Peloton is the Italian group Technogym.

Fund Hunter's approach is simple: good funds own goods stocks. This requires an understanding of what makes a good stock and what makes a bad stock.

I therefore take a look at stocks from time to time. Peloton (PTON) appears to be a bad stock while Technogym (TGYM) might be classed as a good stock. Only time will tell.

Investing is about relative decisions. We have to decide which of the options in front of us is best.

Peloton (PTON) is a tech unicorn and a consumer facing business. We can interact with the product and try to figure out if it is any good.

Technogym is expected to release its Technogym Live home exercise bike in September or October. It will directly compete with the Peloton bike.

Technogym (TGYM) share price €9.4 on 29 August 2019 close; market cap $2bn

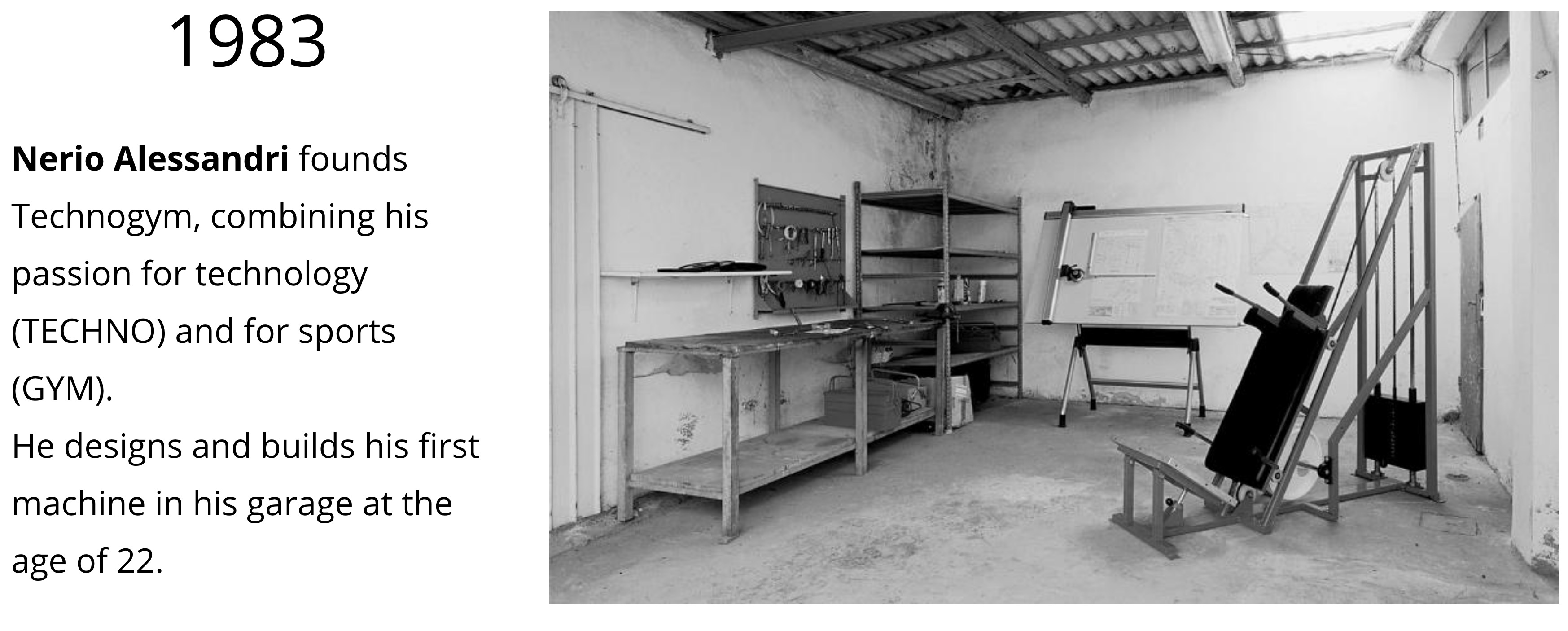

- Leading global fitness equipment brand; founder-led and started in 1984.

- 5% (constant FX) revenue growth in 2018 to $701m; net profit $103m.*

- Technogym Live bike to launch soon; Interim results 10 September.

Peloton (PTON) – last funding round valuation $4bn

- Focus on home exercise bikes with subscription classes; founded in 2012

- Revenue up 119% to $915m in fiscal year in June 2019

- Loss $195.6m in fiscal 2019; $47.8m in 2018 and $71.1m in 2017

* Assuming $1.106/€ Technogym reports in Euros.

My history with Technogym

Technogym is close to my heart. My gym uses Technogym products are recently had them all upgraded. In my view, Technogym equipment offers Italian design, innovation and ease of use.

At my previous employer, I added the shares to our model portfolio at €3.86 on 21 May 2016 – the IPO was May 2016 at €3.25. With the stock currently trading at €9.4, this helps explain the soft spot I have for the group.

I recently visited the Technogym showroom at Harrods in London. This showcases their higher-end products along with the standard lines.

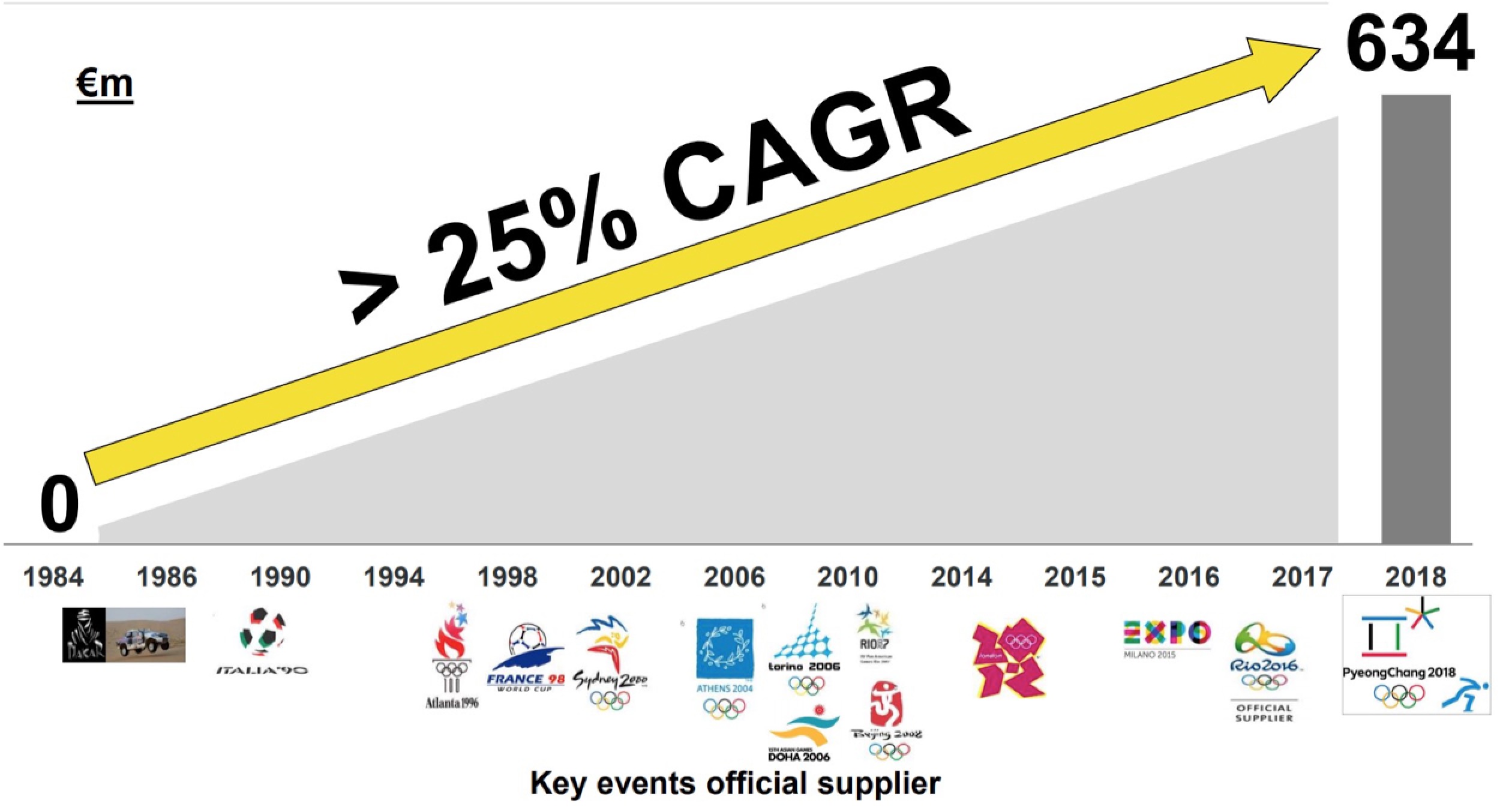

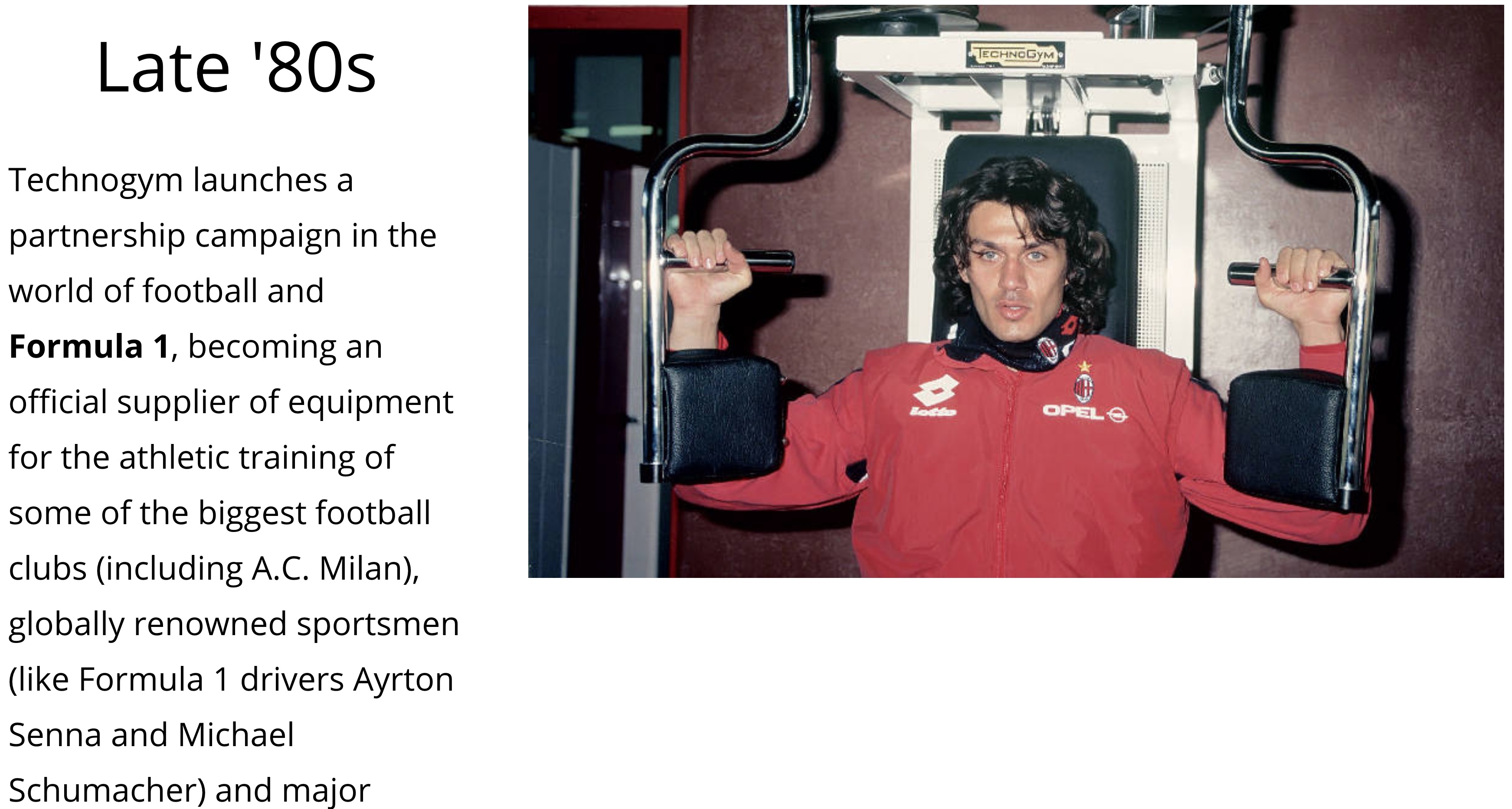

Technogym has a 35-year track record of organic growth

Source: Technogym

Technogym has grown revenue at a compound annual growth rate of over 25% since inception in 1984. While the pace of growth has recently slowed the long-term outlook remains positive.

One research firm expects the global fitness equipment market to increase from US$18.6bn in 2019 to US$29.9bn in 2026. A 60% increase or a compound annual growth rate of 6.2%.

A Peloton competitor

Technogym is soon set to compete directly with Peloton. The Technogym Live home exercise bike with live classes is expected to launch in September or October, according to Technogym representatives.

Technogym Live will partner with local gyms. The group has partnered with 1Rebel in the UK, for example. This may offer a good selling point with the live gym classes having more of a buzz than an instructor in a film studio.

With Peloton seeking to IPO, a leading gym equipment group is set to launch a rival product.

It is not clear what the commercial relationship between Technogym and the gyms it partners with will be. Technogym should be able to earn a meaningful share of the subscription revenue that customers pay to access live classes.

Technogym Live bike: soon to be launched

Source: Technogym

The Peloton bike: pretty good looking

Source: SharePad

One-trick ponies need a good trick

Peloton is a one-trick pony with nearly all its revenue generated from its home exercise bike and related services. The company has launched a home treadmill but demand for this product is likely to be limited.

Consumers may be able to fit an exercise bike in their home but not many are able to fit in a treadmill.

Peloton serves a relatively niche market. Consumers need to be into exercise bikes, have enough space for one and be willing to forgo a gym. The Peloton bike doesn’t appear to be a mass-market product.

Technogym, by contrast, benefits from the growth of gyms around the world. Premium hotels and new apartment blocks all need to have gyms. The number of fitness clubs continues to grow, not least at the budget end of the market.

Technogym also launched its first product into the rehabilitation market in 1992. This may have helped Technogym win a recent contract with the UK gym and private hospital group Nuffield.

Technogym’s Skill Line product category

Source: Technogym

A real business: profits and cash flow

I consider Technogym (TGYM) to be the anti-Peloton because it is both profitable and diversified. Technogym also has a long-established brand with the group the official equipment supplier to the Olympics in recent years.

Technogym is arguably the world’s leading premium gym equipment company.

The brand may not be well known in North America, though, with this segment geography generating only 12% of Technogym revenue in 2018. It was the group’s fastest growing market with 17.3% revenue growth last year.

Technogym may have a good shot at making it big in America.

Europe generated 61% of revenue for the group in 2018 and revenue growth was 10%. If Technogym can repeat its success in Europe around the world then the future is bright.

It is clear from the financial numbers that Technogym is no Unicorn - a start-up that is worth more than $1bn. This is because it is a profitable business generating free cash flow. Unicorns tend to burn through cash.

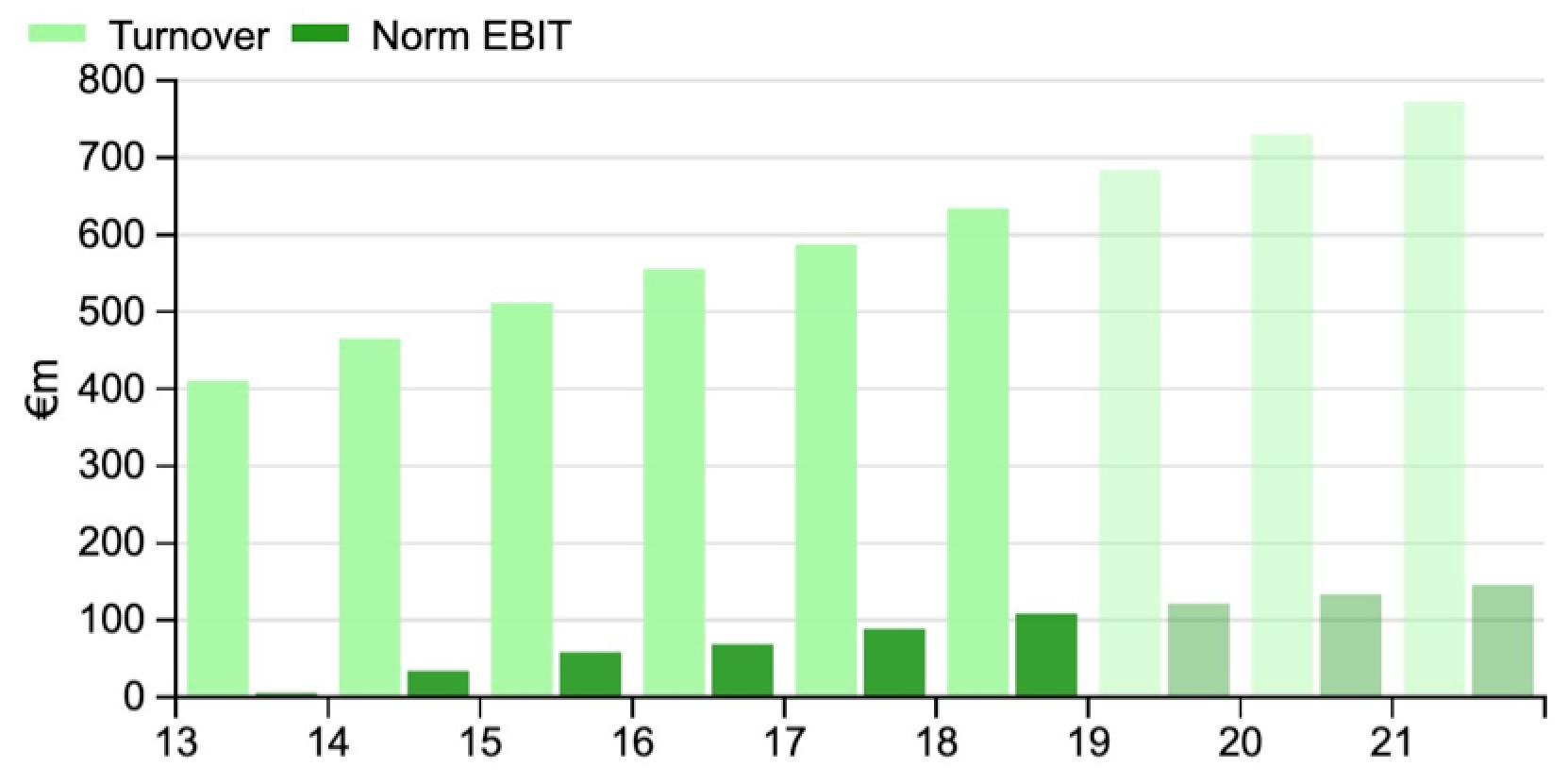

Free cash flow conversion is forecast to be 144% in 2019, 97.5% in 2020 and 99% in 2021. Technogym’s EBIT profit margin has improved from 11.4% in 2015 to 17.1% in 2018 and is expected to make further progress.

Technogym turnover and EBIT profit

Source: SharePad

Revenue and costs

The problem with Peloton’s current revenue is that it may be front-end loaded. A lot of new users are buying Peloton exercise bikes for the first time. They may go on to own them for the next 15 to 20 years before replacing them.

Peloton’s direct-to-consumer model may also be expensive. The group has five stores in London and 69 in the US. Peloton also spends heavily on advertising.

Technogym’s field sales force is tasked with building relationships with gym and hotel chains. The group currently has eight showrooms around the world to promote the brand.

Technogym outlet in Harrods, London - from my undercover trip

Source: My iPhone

Valuation and forecasts

Peloton’s last funding round valued the group at $4bn and the IPO valuation could be as high as $8bn. Technogym is currently valued at US$2bn and is expected to have a net cash position at the end of this year.

Technogym generated $715m revenue in the fiscal year to the end of 2018 and is forecast to generate $757m in 2019. Annual revenue for Peloton was $905m in the fiscal year to June 2018 with subscription revenue a fifth of this figure.

Technogym forecast valuation metrics

Source: SharePad

An additional rival: NOHrD

Another rival is the NOHrD wooden exercise bike. You can use it with a laptop or iPad and watch whatever you want without a subscription.

The problem with the Peloton bike is that unless you subscribe you have a dark screen. You even need a subscription to access scenic cycling routes where an instructor isn't present.

Source: NOHrD

Have you tried a Peloton bike?

The rebuttal to Tesla bears tends to be: have you ridden in the car? On this basis I have tried out a Peloton bike in a showroom in London.

The bike is well designed and the screen is high quality. There is clearly a niche market for the product. But the trouble is that it is likely to remain just that, a niche market.

Peloton's Spitalfields store

Source: my iPhone

Devil’s advocate

It is always useful to consider the alternative view. Peloton’s bike may be able to hold its own against any new competitors. The group has the leading brand and once customers have bought the bike they are locked into the service.

As Peloton scales up it may see a rapid improvement in profitability. This is because the group’s gym and studio costs are fixed. An additional customer pays a subscription fee to access them without a further cost to Peloton.

Marketing costs for Peloton may decline over time in absolute terms and as a percentage of revenue.

Peloton may have tapped into something. A lot of people may want access to a quick and easy exercise class in the comfort of their own home.

Summary

In their latest fiscal years, Peloton reported a US$195.6 million loss while Technogym reported a US$103 net profit. The two companies are very different beasts.

If I had to bet on one, it would be Technogym at €9.4 and I would avoid Peloton at its IPO price. It will be interesting to check back in a few years time to see how this prediction plays out.

Technogym is set to launch a product that competes with the Peloton bike in the coming months. They may or may not be successful. What is clear is that Technogym is an established business with a positive long-term outlook.

The medium-term outlook is less certain with demand for fitness equipment not exactly recession proof.

Technogym share price since the IPO

Source: SharePad

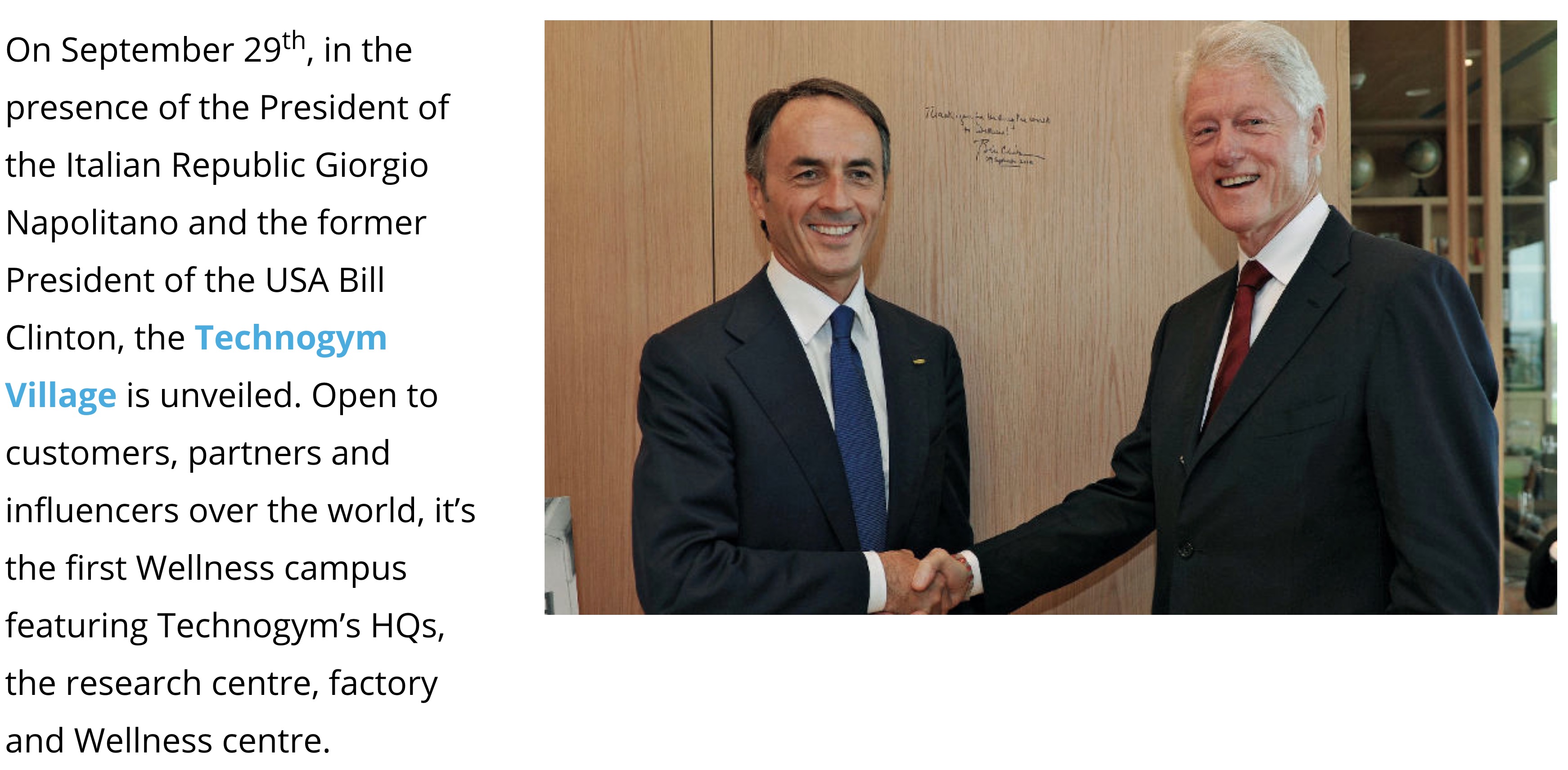

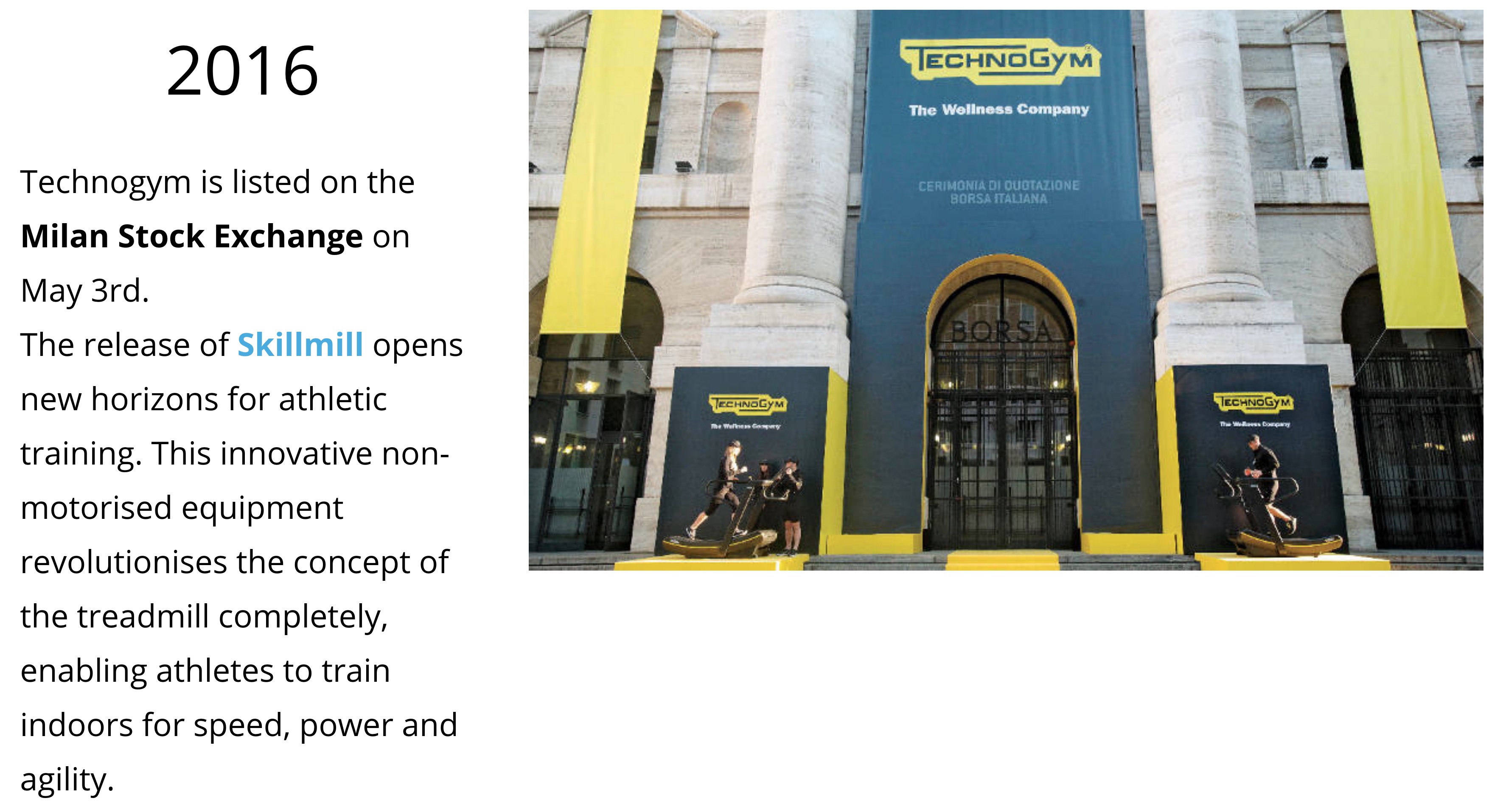

Technogym's history in four photos

Technogym founder Nerio Alessandri with Bill Clinton

2012

Source: Technogym